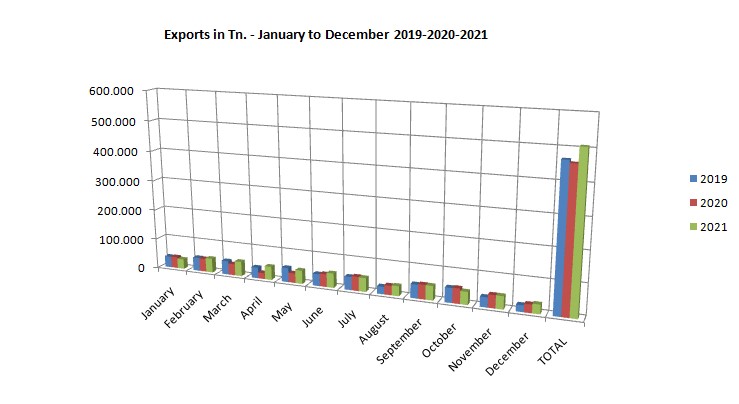

1 – Global Exports – January to December 2021

December is usually characterised by a slowdown in activity due to the closure of factories for Christmas and a reduction in demand (stocking period in warehouses). However, this is not the case this year. Activity has not slowed down as one might expect. As the results for 2021 show compared to 2019 and 2020, it could not be better: +10.67% (2020-2021) and +8.60% (2019-2021), i.e. a total of 508,176 tonnes of slate exported.

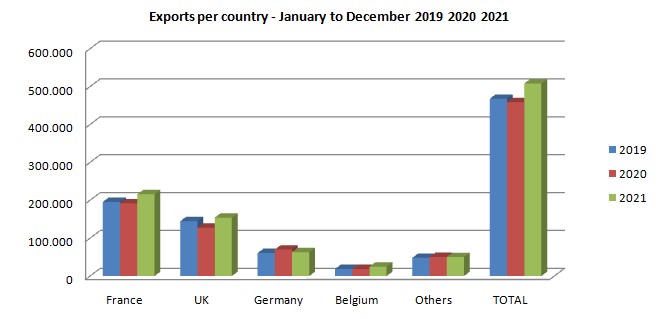

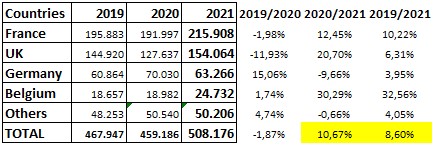

2 – Analysis by country.

France remains the main importer with 215 908 tonnes. This volume is practically equivalent to that achieved by England and Germany combined, even if, as can be seen, the growth of the English market remains very strong.

The reasons for these results have already been explained on other occasions:

– The strength of the slate tradition in France, a country that can be considered a pioneer in the industrial production of this material for centuries until the closure of its last quarries;

– The competitiveness of Spanish slate in terms of quantity and quality compared to other alternative roofing materials;

– The strength of slate as a natural product, a label that is increasingly appreciated by the market, which considers the importance of ecology in particular;

– The growing demand created after the pandemic. The property sector continues to consolidate as a safe haven for investment, reinforced in this case by the strength of savings in the family economy;

The UK: exports continue to grow steadily without the feared effects of Brexit being felt. To date, they have almost doubled the tonnes achieved ten years ago, making it the second most important market, far exceeding the German market;

Germany: the results of the 2019-2021 comparison are very similar, a very stable and regular market, without the excitement of the French or English market;

Belgium, whose market is smaller due to a less dense population, stands out this year with a remarkable increase of 32.56% (from 18,657 tonnes in 2019 to 24,732 tonnes in 2021);

In summary, 2021 was a very positive year, albeit with nuances due to the sharp rise in production costs. In fact, the impact on the prices of energy, fuel, wood and logistics is causing an undesirable inflationary spiral in the slate, as in the case of the rest of the raw materials, as it may affect the competitiveness of our product and penalise the projects underway. We continue to point out, in the light of the statistics, a certain weakness in the sector’s production capacity, because even though we are in a context of high demand (perhaps the highest in history) and with practically empty stocks, the overall increase in sales between 2019 and 2021 is only 8.60% (we prefer not to compare the data for 2020 because the figures are altered by the pandemic and production stoppages due to the lock-in).

In principle, the year 2022 promises to continue the same trend: high demand with high delivery times due to the minimum stock available. Unfortunately, the constant increases in costs will continue, aggravated this time by the conflict between Russia and Ukraine, which is already having a major impact on the prices of all raw materials and jeopardising our price control policy.

Source: Clúster de la pizarra de Galicia – February 2022.